Shipbuilding Market Valued at USD 162.14 Billion in 2024, Set for Continued Growth

Global Shipbuilding Market: Industry Overview and Forecast (2025–2032)

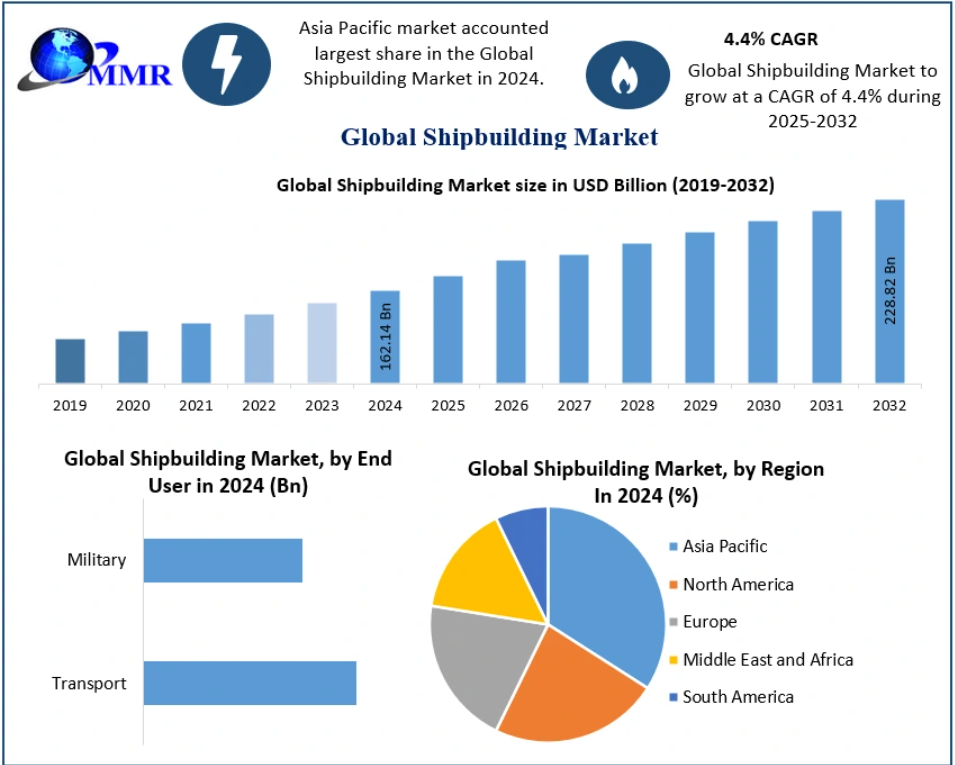

The Global Shipbuilding Market was valued at USD 162.14 billion in 2024 and is projected to reach nearly USD 228.82 billion by 2032, growing at a CAGR of 4.4% during the forecast period. The market’s expansion is primarily driven by the steady rise in international seaborne trade, increased defense budgets, and continuous technological advancements in vessel design and marine engineering.

Market Overview

Shipbuilding refers to the construction of ships and other floating structures, typically carried out in specialized facilities known as shipyards. The craft of shipbuilding, practiced by shipwrights, has evolved from traditional, experience-based techniques to a high-tech discipline combining engineering precision, material science, and hydrodynamics.

Modern shipbuilding serves both commercial and military sectors, covering the production of cargo vessels, tankers, passenger ships, and naval warships. The rapid expansion of maritime logistics, combined with the demand for more fuel-efficient and autonomous vessels, continues to reshape the industry landscape.

Gain insights into the most attractive segments — click here to receive a free sample of the report:https://www.maximizemarketresearch.com/request-sample/148775/

Impact of COVID-19

The COVID-19 pandemic caused severe disruptions in global shipbuilding operations. Lockdowns, restricted workforce mobility, and supply chain breakdowns halted shipyard activities worldwide. Major shipbuilders, including Samsung Heavy Industries and Irving Shipbuilding, temporarily closed operations, leading to significant revenue losses and project delays.

However, post-pandemic recovery initiatives and renewed global trade activity have restored market momentum. Governments’ focus on sustaining maritime trade and upgrading naval capabilities has also provided a much-needed boost to the sector’s recovery.

Market Dynamics

Key Growth Drivers

-

Rising Seaborne Trade and Economic Growth

More than 80% of global trade volume is carried by sea. The rapid globalization of supply chains and increased import-export activities are driving demand for new vessels, especially in Asia and Europe. -

Technological Advancements and Automation

The integration of automation, digital twin technology, AI-based navigation, and IoT-enabled fleet management is improving operational efficiency, reducing maintenance costs, and enhancing ship safety. -

Defense and Security Expansion

Growing geopolitical tensions and maritime security challenges have increased investments in naval modernization programs, driving the demand for military shipbuilding. -

Economic and Industrial Expansion

Rising industrialization and GDP growth in emerging economies have amplified demand for bulk carriers and container ships to facilitate trade in raw materials and consumer goods.

Market Restraints

-

High Capital and Maintenance Costs: Shipbuilding requires significant investment in infrastructure, skilled labor, and materials.

-

Environmental Regulations: Strict global emissions standards, including IMO 2020, are pushing shipbuilders to adopt cleaner technologies, increasing production costs.

-

Volatile Raw Material Prices: Fluctuating steel and fuel prices continue to challenge profitability across shipyards.

Market Opportunities

-

Autonomous and Smart Ships: Growing investments in unmanned vessel technology present a major growth avenue.

-

Green Shipbuilding Initiatives: Rising adoption of eco-friendly designs and renewable energy propulsion systems, such as LNG and hydrogen fuel, are opening new market opportunities.

-

Defense Collaboration Projects: Cross-border defense partnerships are leading to new shipbuilding contracts for naval fleets.

Market Segmentation

By Type

-

Oil Tankers – Expected to witness consistent demand due to the global oil trade.

-

Bulk Carriers – Driven by industrial raw material transport such as coal, ore, and grains.

-

Cargo Ships – Anticipated to register the highest CAGR due to the growing e-commerce-driven logistics sector.

-

Container Ships – Supported by global trade expansion and advancements in fuel-efficient vessel design.

-

Passenger Ships – Growth fueled by increasing maritime tourism and luxury cruise demand.

By End User

-

Transport – Dominates the market, driven by the surge in global commercial shipping and tourism.

-

Military – Growing defense expenditure and modernization programs are boosting naval shipbuilding demand worldwide.

Regional Insights

Asia-Pacific (APAC): Market Leader

The Asia-Pacific region accounted for nearly 82% of global market share in 2024, making it the undisputed leader in shipbuilding. China, Japan, and South Korea dominate global production, with China capturing over 50% of total new ship orders.

South Korea’s shipbuilders, including Hyundai Heavy Industries, DSME, and Samsung Heavy Industries, focus on high-value segments such as LNG carriers and specialized vessels.

Additionally, India, Bangladesh, and Pakistan have emerged as global leaders in ship recycling, handling nearly 90% of global ship scrapping.

Europe

Europe remains a key region, particularly for cruise ship and defense vessel manufacturing. Recent contracts, including Daewoo Shipbuilding’s $1.5 billion order from European shipping companies, highlight the region’s strong market position in high-specification vessels.

North America

North America’s shipbuilding market is driven by naval expansion programs and offshore energy development, particularly in the U.S. defense and energy sectors.

Middle East & Africa / South America

Emerging regions are increasingly investing in port infrastructure and maritime defense capabilities, creating long-term opportunities for shipbuilders and component suppliers.

Gain insights into the most attractive segments — click here to receive a free sample of the report:https://www.maximizemarketresearch.com/request-sample/148775/

Competitive Landscape

The global shipbuilding market is moderately consolidated, with a mix of established international players and regional shipyards focusing on niche segments. Key players are investing in automation, digital shipyard solutions, and sustainability-driven designs to enhance competitiveness.

Key Companies:

-

Raytheon Technologies Corporation

-

Huntington Ingalls Industries, Inc.

-

General Dynamics Corporation

-

Damen Shipyards Group

-

BAE Systems

-

STX Offshore & Shipbuilding Co., Ltd.

-

Sumitomo Heavy Industries, Ltd.

-

FINCANTIERI S.p.A.

-

China State Shipbuilding Corporation Limited (CSSC)

-

DSME Co., Ltd.

-

China Shipbuilding Industry Corporation (CSIC)

-

United Shipbuilding Corporation

-

Larsen & Toubro Limited

-

NorthStar Shipbuilding Pvt. Ltd.

-

Tsuneishi Shipbuilding Co., Ltd.

Future Outlook

The shipbuilding industry is transitioning toward a digitally integrated and environmentally sustainable future. The adoption of green propulsion systems, AI-driven navigation, and autonomous vessels will shape the next generation of ship design and manufacturing.

Between 2025 and 2032, global demand is expected to remain strong, particularly for energy-efficient cargo ships and defense vessels. As global trade rebounds and sustainability becomes a core focus, the shipbuilding market will remain a cornerstone of international commerce and defense innovation.

Sponsor

Sponsor

Categorieën

- AI

- Ontwerp

- Fashion and Art

- Investment and Finance

- Top 10

- Christianity

- Climate and Enviroment

- Writing and Film

- Fitness

- Food

- Spellen

- Gardening

- Health

- Home and Interiors

- Marketing and Sales

- Music

- Making Money Online

- Others

- Books

- Religion

- Ecommerce

- Sports

- Cars

- Wellness

- Tech Gadgets

- Events

- Governments and Nations

- Science and Engineering

- Real Estate

- Travel, Tourism and Hospitality

- Onderwijs

- Startups

- Beauty and Cosmetics

- Agriculture

- Computer Operating Systems

- Crypto

- Politics and News

- Video Review

- Immigration

Read More

PHILADELPHIA For Mets supervisor Carlos Mendoza, 1 of the highest critical discussions of each individual working day is the a person with his nearer. For 5 and a 50 % weeks, the Mets handled Edwin Díaz cautiously, not seeking towards overtax his surgically fixed specifically knee nor his golden straight arm. That transformed just about right away in just late September, Even though...

Future of Executive Summary Surge Protection Devices Market: Size and Share Dynamics Surge protection devices market is expected to gain market growth in the forecast period of 2022 to 2029. Data Bridge Market Research analyses the surge protection devices market to exhibit a CAGR of 5.50% for the forecast period of 2022 to 2029. Businesses can attain detailed insights with the large scale...

Executive Summary Middle East and Africa Flat Glass Market Size and Share Forecast CAGR Value: Data Bridge Market Research analyses that the flat glass market is expected to reach USD 15253.95 million by 2030, which is USD 8552.92 million in 2022, registering a CAGR of 7.50% during the forecast period of 2023 to 2030. Middle East and Africa Flat Glass Market business report...

Printed Electronics Market size was valued at USD 13.47 Bn. in 2023 and the total Printed Electronics revenue is expected to grow by 17.3% from 2024 to 2030, reaching nearly USD 41.18 Bn. Printed Electronics Market Overview Maximize Market Research is a research firm. They provided an in-depth analysis of the "Printed Electronics Market". The analysis includes price considerations,...

Comprehensive Outlook on Executive Summary Edible Packaging Market Size and Share Global edible packaging market size was valued at USD 688.76 million in 2024 and is projected to reach USD 1057.04 million by 2032, with a CAGR of 5.50% during the forecast period of 2025 to 2032. Edible Packaging Market research report unearths different industry verticals such as company profile,...