Global Automotive Wire and Cable Market Size to Reach USD 32,090 Million by 2032, Growing at a CAGR of 3.6%

MARKET INSIGHTS

The global automotive wire and cable market size was valued at USD 25,250 million in 2024. The market is projected to grow from USD 26,150 million in 2025 to USD 32,090 million by 2032, exhibiting a CAGR of 3.6% during the forecast period.

Report Sample includes:

- Table of Contents

- List of Tables & Figures

- Charts

- Research Methodology

Get FREE Sample of this Report at https://www.intelmarketresearch.com/download-free-sample/13372/automotive-wirecable-market

Automotive wires and cables are fundamental components of a vehicle's electronic control system. These assemblies, which are often bonded, twisted, or braided together, form the central nervous system of a modern automobile, transmitting electric power, data, and signals for functions ranging from infotainment to critical safety systems. Because they operate in harsh under-hood environments, these components must possess specialized characteristics, most notably high-temperature resistance, to ensure reliability and safety.

Market growth is primarily driven by the increasing electrification of vehicles and the rising adoption of advanced driver-assistance systems (ADAS), which require more complex and robust wiring harnesses. However, the industry faces challenges from the volatility of raw material prices, particularly copper. The market is highly concentrated, with the top three manufacturers Yazaki Corporation, Sumitomo Electric, and Aptiv collectively holding a dominant share of approximately 60%. Geographically, Europe is the largest market with a share of about 23%, while the combined markets of Japan and China account for over 40% of global demand.

Accelerated Vehicle Electrification to Drive Automotive Wire and Cable Demand

The global shift toward vehicle electrification represents the most significant growth driver for automotive wire and cable markets. Electric vehicles require substantially more wiring content than conventional internal combustion engine vehicles, with premium EVs containing over 5,000 meters of wiring compared to approximately 1,500 meters in traditional vehicles. This increased complexity stems from the sophisticated battery management systems, extensive sensor networks, and advanced power distribution requirements unique to electric powertrains. Government mandates pushing for electrification, including the European Union's 2035 ban on new internal combustion engine vehicles and similar initiatives across North America and Asia-Pacific, are creating sustained demand for high-performance automotive wiring systems capable of handling higher voltages and more complex data transmission requirements.

Advanced Driver Assistance Systems (ADAS) Expansion to Boost Market Growth

The proliferation of Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies is creating unprecedented demand for specialized automotive cables capable of handling high-speed data transmission. Modern vehicles increasingly incorporate radar systems, LiDAR sensors, camera networks, and ultrasonic sensors that require reliable data connectivity with minimal latency. The transition toward higher levels of autonomy necessitates wiring systems that can support data rates exceeding 10 Gbps for sensor fusion and real-time decision-making. This technological evolution drives demand for shielded twisted pair cables, coaxial cables, and fiber optic solutions that can maintain signal integrity in challenging automotive environments while resisting electromagnetic interference.

Growing Vehicle Connectivity Features to Fuel Wiring System Requirements

The integration of comprehensive connectivity features in modern vehicles is substantially increasing the complexity and volume of automotive wiring systems. Contemporary vehicles function as connected platforms requiring extensive networking capabilities for telematics, infotainment, vehicle-to-everything (V2X) communication, and over-the-air updates. This connectivity revolution demands robust wiring architectures that can support multiple communication protocols including CAN, LIN, FlexRay, Automotive Ethernet, and MOST. The average premium vehicle now contains more than 100 electronic control units interconnected through complex wiring networks, creating sustained demand for specialized cables that can handle both power distribution and high-speed data communication while meeting automotive-grade reliability standards.

MARKET RESTRAINTS

Raw Material Price Volatility to Constrain Market Stability

The automotive wire and cable market faces significant challenges from fluctuating raw material prices, particularly copper, which constitutes approximately 60-70% of wiring harness material costs. Copper prices have demonstrated considerable volatility in recent years, influenced by global supply chain disruptions, mining production fluctuations, and geopolitical factors. This price instability creates manufacturing cost uncertainties and margin pressures for wire harness producers who typically operate on long-term contracts with automotive OEMs. The industry's transition toward aluminum alternatives, while providing cost reduction opportunities, introduces technical challenges regarding conductivity, durability, and connection reliability that require substantial research and development investment to overcome.

Increasing Wiring Complexity to Challenge Manufacturing Efficiency

While technological advancements drive market growth, they simultaneously create manufacturing challenges through increasing wiring system complexity. Modern vehicle architectures require more intricate wiring layouts with greater numbers of connections, specialized shielding requirements, and reduced tolerances for error. This complexity escalates production costs, extends manufacturing timelines, and increases the potential for quality issues. The automotive industry's transition to zone-based E/E architectures, while simplifying overall wiring, requires more sophisticated central computing units and higher-performance cabling, presenting manufacturing challenges related to precision assembly, testing protocols, and workforce training requirements.

Weight Reduction Pressures to Limit Traditional Wiring Applications

Automotive manufacturers face increasing pressure to reduce vehicle weight for improved fuel efficiency and extended electric vehicle range, creating restraints for traditional wiring systems. Wiring harnesses represent one of the heaviest components in modern vehicles, with premium vehicles containing over 50 kilograms of wiring. This weight concern drives OEMs to seek alternative solutions including aluminum wiring, fiber optics, and optimized wiring architectures that reduce copper content. However, these alternatives often come with trade-offs regarding performance, durability, and manufacturing compatibility, creating implementation challenges that restrain market growth for conventional wiring solutions while stimulating innovation in lightweight alternatives.

MARKET CHALLENGES

Supply Chain Fragility to Challenge Production Consistency

The automotive wire and cable market faces persistent challenges from fragile global supply chains that have demonstrated vulnerability to disruptions. The industry's just-in-time manufacturing model depends on reliable component delivery, and wiring harness production requires numerous specialized materials including copper, insulation compounds, connectors, and shielding materials. Recent global events have exposed vulnerabilities in this supply network, causing production delays and cost increases. The geographical concentration of wiring harness manufacturing in specific regions creates additional risk, as natural disasters, geopolitical tensions, or logistical disruptions in these areas can significantly impact global automotive production.

Other Challenges

Technological Standardization Issues

The rapid evolution of automotive technologies creates challenges regarding standardization across the industry. Different manufacturers adopt varying approaches to wiring architectures, communication protocols, and connection systems, resulting in compatibility issues and increased complexity for suppliers. The absence of universal standards for high-voltage cabling in electric vehicles, data communication protocols for advanced driver assistance systems, and connection interfaces for new electronic components creates development uncertainties and increases research and development costs for wire harness manufacturers serving multiple OEM customers.

Environmental Compliance Requirements

Increasing environmental regulations present significant challenges for wire and cable manufacturers regarding material composition, production processes, and end-of-life management. Restrictions on hazardous substances, requirements for recyclability, and mandates for sustainable sourcing create compliance complexities that affect material selection and manufacturing methodologies. The industry must balance performance requirements with environmental considerations, often requiring substantial investment in alternative materials, production technologies, and recycling infrastructure to meet evolving regulatory standards across different global markets.

MARKET OPPORTUNITIES

High-Voltage Cable Systems for Electric Vehicles to Create Expansion Opportunities

The accelerating transition to electric vehicles presents substantial growth opportunities for high-voltage cable systems capable of handling increased power requirements. Electric vehicles require specialized cabling for battery connections, charging systems, and power distribution that can safely manage voltages exceeding 800 volts in advanced platforms. This creates demand for cables with enhanced insulation properties, superior thermal management capabilities, and improved durability characteristics. The development of ultra-fast charging technologies further drives requirements for cables that can maintain performance under extreme electrical loads while ensuring safety and reliability throughout the vehicle's operational life.

Automotive Ethernet Adoption to Drive Next-Generation Data Cable Demand

The automotive industry's increasing adoption of Ethernet-based networks creates significant opportunities for advanced data cables supporting higher bandwidth requirements. As vehicles evolve into software-defined platforms with extensive connectivity features, the demand for reliable high-speed data transmission grows exponentially. Automotive Ethernet cables capable of supporting multi-gigabit data rates enable advanced infotainment systems, enhanced driver assistance features, and vehicle-to-cloud connectivity. This technological shift requires specialized cabling solutions that combine data transmission performance with automotive environmental robustness, creating opportunities for manufacturers developing cables that meet both technical specifications and automotive reliability standards.

Lightweight Material Innovation to Open New Market Segments

The ongoing pursuit of vehicle weight reduction creates opportunities for innovative lightweight cable solutions that maintain performance while reducing mass. Development of aluminum-based wiring systems, composite conductors, and optimized insulation materials addresses the automotive industry's need for weight savings without compromising electrical performance or durability. These innovations are particularly valuable for electric vehicles, where weight reduction directly impacts range capability and overall efficiency. The market opportunity extends beyond material development to include design innovations that reduce overall wiring content through architectural improvements, smarter routing, and integration of multiple functions into single cable systems.

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The competitive landscape of the global automotive wire and cable market is highly consolidated, dominated by a few major players who collectively hold a significant market share. According to industry analysis, the top three manufacturers Yazaki Corporation, Sumitomo Electric Industries, and Aptiv PLC collectively account for approximately 60% of the global market revenue. This concentration is primarily due to their extensive product portfolios, longstanding relationships with global automakers, and robust manufacturing and distribution networks across key automotive-producing regions.

Yazaki Corporation maintains its leadership position through continuous innovation in high-temperature resistant and lightweight wiring systems, catering to the increasing electrification and automation in vehicles. Similarly, Sumitomo Electric leverages its expertise in material science to develop advanced aluminum core cables that reduce vehicle weight and improve fuel efficiency, aligning with stringent global emission norms. Aptiv focuses on data transmission cables for advanced driver-assistance systems (ADAS) and in-vehicle networking, securing its role as a critical supplier in the evolving automotive electronics space.

Meanwhile, other established players like Leoni AG and Furukawa Electric are strengthening their market presence through significant investments in research and development and strategic expansions into emerging markets. These companies are actively developing solutions for electric vehicles (EVs), including high-voltage cables and charging systems, to capture growth in this rapidly expanding segment. Their efforts in forming joint ventures and technological partnerships with automakers ensure they remain integral to the industry's supply chain.

The market also features strong regional competitors, particularly in Asia, where companies like Kyungshin (South Korea) and Yura Corporation (South Korea) have carved out substantial shares due to their proximity to major automotive manufacturing hubs and cost-effective production capabilities. In China, players such as Huguang Auto Harness and JinTing Automobile Harness are growing rapidly, supported by the domestic automotive boom and government initiatives promoting new energy vehicles.

Overall, competition is intensifying as companies not only compete on price and quality but also on their ability to innovate and provide integrated solutions for next-generation vehicles. The focus on sustainability, such as developing recyclable materials and reducing the environmental footprint of production processes, is becoming a differentiator in this competitive arena.

List of Key Automotive Wire and Cable Companies Profiled

Yazaki Corporation (Japan)

Sumitomo Electric Industries, Ltd. (Japan)

Aptiv PLC (Ireland)

Leoni AG (Germany)

Lear Corporation (U.S.)

Furukawa Electric Co., Ltd. (Japan)

Dräxlmaier Group (Germany)

Kromberg & Schubert GmbH (Germany)

Coficab Group (Tunisia)

Kyungshin Corporation (South Korea)

Yura Corporation (South Korea)

Fujikura Ltd. (Japan)

Motherson Group (India)

Shuangfei Auto Electric Appliances Co., Ltd. (China)

Huguang Auto Harness Co., Ltd. (China)

JinTing Automobile Harness Co., Ltd. (China)

Yazaki Corporation (Japan)

Sumitomo Electric Industries, Ltd. (Japan)

Aptiv PLC (Ireland)

Leoni AG (Germany)

Lear Corporation (U.S.)

Furukawa Electric Co., Ltd. (Japan)

Dräxlmaier Group (Germany)

Kromberg & Schubert GmbH (Germany)

Coficab Group (Tunisia)

Kyungshin Corporation (South Korea)

Yura Corporation (South Korea)

Fujikura Ltd. (Japan)

Motherson Group (India)

Shuangfei Auto Electric Appliances Co., Ltd. (China)

Huguang Auto Harness Co., Ltd. (China)

JinTing Automobile Harness Co., Ltd. (China)

The global push towards vehicle electrification represents the most significant driver for the automotive wire and cable market. With major economies and automotive manufacturers committing to an electric future, the demand for sophisticated wiring harnesses has surged dramatically. Battery Electric Vehicles (BEVs) and Plug-in Hybrid Electric Vehicles (PHEVs) require substantially more wiring than traditional internal combustion engine vehicles due to complex battery management systems, extensive sensor networks, and high-voltage power distribution. This shift is not merely a trend but a fundamental restructuring of the automotive industry, directly translating into a higher volume of wire and cable consumption per vehicle. The market is responding with innovations in high-voltage cable technology capable of handling up to 900 volts to support faster charging capabilities and more powerful electric drivetrains.

Other Trends

Integration of Advanced Driver-Assistance Systems (ADAS)

The rapid integration of Advanced Driver-Assistance Systems (ADAS) and autonomous driving features is creating a substantial demand for high-speed data transmission cables within vehicles. Modern vehicles are evolving into data centers on wheels, equipped with a multitude of sensors, cameras, radar, and LiDAR systems. This ecosystem requires robust and reliable data cabling, such as coaxial cables and shielded twisted pairs, to handle the immense bandwidth necessary for real-time data processing. The proliferation of these features, from adaptive cruise control to lane-keeping assistance, is no longer confined to luxury segments and is becoming standard in mid-range vehicles, further accelerating the need for advanced and reliable wire and cable solutions that ensure signal integrity and electromagnetic compatibility.

Lightweighting and Material Innovation

The automotive industry's relentless focus on improving fuel efficiency and extending the range of electric vehicles is driving the trend of lightweighting, which extends directly to wire harnesses. Manufacturers are increasingly adopting aluminum-based cables as a lighter and more cost-effective alternative to traditional copper, despite its different electrical properties. Furthermore, there is significant development in the insulation materials used. Polyvinyl chloride (PVC) is being supplemented or replaced by materials like cross-linked polyethylene (XLPE) and thermoplastic elastomers (TPE) that offer superior resistance to high temperatures, abrasion, and chemicals while being lighter. This material innovation is critical for ensuring reliability in the harsh under-hood environment of modern vehicles, particularly those with high-temperature engines and components found in hybrids and EVs.

Europe Europe represents the largest regional market for automotive wire and cable, accounting for approximately 23% of global demand. This leadership position is driven by the region's advanced automotive manufacturing sector, stringent regulatory standards for vehicle safety and emissions, and high adoption of electric and connected vehicle technologies. Germany stands as the dominant market within Europe, supported by its robust automotive OEM presence and strong focus on innovation in automotive electronics. The region's emphasis on lightweight materials and high-temperature resistant cables aligns with evolving vehicle electrification trends and performance requirements. Regulatory framework

European Union regulations, including strict emissions standards and vehicle safety directives, mandate advanced wiring systems that support complex electronic controls and energy efficiency. Compliance with these standards necessitates high-quality, durable cables capable of withstanding extreme automotive environments. Market leadership

Germany's automotive industry, home to major OEMs and suppliers, drives significant wire and cable consumption. The presence of global leaders like Leoni AG and Kromberg & Schubert further consolidates Europe's influence in manufacturing advanced automotive wiring harnesses and related components. Growth drivers

Rising production of electric vehicles (EVs) and hybrid models requires specialized high-voltage cables and enhanced data transmission capabilities. Increased integration of ADAS (Advanced Driver Assistance Systems) and infotainment systems also fuels demand for sophisticated wire and cable solutions across European automotive platforms. Challenges

High material costs, particularly for copper, and supply chain complexities pose challenges to market growth. Intense competition from Asian manufacturers and the need for continuous innovation in material science also pressure European suppliers to maintain technological leadership while managing cost efficiencies.

Asia-Pacific

Asia-Pacific is the highest volume-consuming region for automotive wire and cable, driven largely by automotive production hubs in China, Japan, and South Korea. Combined, these countries account for over 40% of global demand. The region benefits from extensive manufacturing infrastructure, cost-competitive supply chains, and growing investments in electric vehicle production. While conventional wiring systems remain prevalent due to cost considerations, increasing regulatory focus on vehicle safety and emissions is accelerating adoption of advanced, high-performance cables across the region.

North America

North America's automotive wire and cable market is characterized by high technological adoption and a shift toward electric and autonomous vehicles. The United States is the largest contributor, supported by a resurgence in automotive manufacturing and investments in modernizing vehicle fleets. Demand is driven by the need for reliable, high-temperature resistant cables suitable for increasingly electronic-intensive vehicles, including trucks, SUVs, and emerging EV models from both traditional and new automotive manufacturers.

South America

The South American market is developing, with growth opportunities linked to regional automotive production expansions, particularly in Brazil and Argentina. However, economic volatility and fluctuating automotive production volumes moderate more rapid adoption of advanced wiring systems. Cost sensitivity remains a key factor, though increasing safety standards and gradual electrification trends are expected to support long-term market development.

Middle East & Africa

This region represents an emerging market with potential growth driven by gradual industrialization and increasing vehicle ownership. Infrastructure development and economic diversification in countries like Saudi Arabia and the UAE are fostering automotive sector growth. Nonetheless, the market remains challenged by limited local manufacturing and reliance on imports, slowing the adoption of advanced automotive wire and cable technologies in the short term.

This market research report offers a holistic overview of global and regional markets for the forecast period 2025â2032. It presents accurate and actionable insights based on a blend of primary and secondary research.

Key Coverage Areas:

â Market Overview

Global and regional market size (historical & forecast)

Growth trends and value/volume projections

â Segmentation Analysis

By product type or category

By application or usage area

By end-user industry

By distribution channel (if applicable)

â Regional Insights

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

Country-level data for key markets

â Competitive Landscape

Company profiles and market share analysis

Key strategies: M&A, partnerships, expansions

Product portfolio and pricing strategies

â Technology & Innovation

Emerging technologies and R&D trends

Automation, digitalization, sustainability initiatives

Impact of AI, IoT, or other disruptors (where applicable)

â Market Dynamics

Key drivers supporting market growth

Restraints and potential risk factors

Supply chain trends and challenges

â Opportunities & Recommendations

High-growth segments

Investment hotspots

Strategic suggestions for stakeholders

â Stakeholder Insights

Target audience includes manufacturers, suppliers, distributors, investors, regulators, and policymakers

â Market Overview

Global and regional market size (historical & forecast)

Growth trends and value/volume projections

Global and regional market size (historical & forecast)

Growth trends and value/volume projections

â Segmentation Analysis

By product type or category

By application or usage area

By end-user industry

By distribution channel (if applicable)

By product type or category

By application or usage area

By end-user industry

By distribution channel (if applicable)

â Regional Insights

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

Country-level data for key markets

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

Country-level data for key markets

â Competitive Landscape

Company profiles and market share analysis

Key strategies: M&A, partnerships, expansions

Product portfolio and pricing strategies

Company profiles and market share analysis

Key strategies: M&A, partnerships, expansions

Product portfolio and pricing strategies

â Technology & Innovation

Emerging technologies and R&D trends

Automation, digitalization, sustainability initiatives

Impact of AI, IoT, or other disruptors (where applicable)

Emerging technologies and R&D trends

Automation, digitalization, sustainability initiatives

Impact of AI, IoT, or other disruptors (where applicable)

â Market Dynamics

Key drivers supporting market growth

Restraints and potential risk factors

Supply chain trends and challenges

Key drivers supporting market growth

Restraints and potential risk factors

Supply chain trends and challenges

â Opportunities & Recommendations

High-growth segments

Investment hotspots

Strategic suggestions for stakeholders

High-growth segments

Investment hotspots

Strategic suggestions for stakeholders

â Stakeholder Insights

Target audience includes manufacturers, suppliers, distributors, investors, regulators, and policymakers

Target audience includes manufacturers, suppliers, distributors, investors, regulators, and policymakers

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Wire and Cable Market?

-> The global automotive wire and cable market was valued at USD 25,250 million in 2024 and is projected to reach USD 32,090 million by 2032.

Which key companies operate in Global Automotive Wire and Cable Market?

-> Key players include Yazaki Corporation, Sumitomo Electric, Aptiv, Leoni, Lear Corporation, and Furukawa Electric, among others.

What are the key growth drivers?

-> Key growth drivers include increasing vehicle electrification, rising demand for advanced safety features, and growth in automotive production.

Which region dominates the market?

-> Europe is the largest market with approximately 23% share, while Asia-Pacific represents the fastest-growing region.

What are the emerging trends?

-> Emerging trends include development of high-temperature resistant materials, lightweight aluminum wiring solutions, and integration of smart connectivity features.

Get the Complete Report & TOC at https://www.intelmarketresearch.com/automotive-and-transportation/13372/automotive-wirecable-market

CONTACT US:

276 5th Avenue, New York , NY 10001,United States

International: (+1) 646 781 7170

Email: help@intelmarketresearch.com

Follow Us On linkedin :- https://www.linkedin.com/company/24-market-reports

Related Links

Спонсоры

Спонсоры

Категории

- AI

- Дизайн

- Fashion and Art

- Investment and Finance

- Top 10

- Christianity

- Climate and Enviroment

- Writing and Film

- Fitness

- Food

- Игры

- Gardening

- Health

- Home and Interiors

- Marketing and Sales

- Music

- Making Money Online

- Others

- Books

- Religion

- Ecommerce

- Sports

- Cars

- Wellness

- Tech Gadgets

- Мероприятия

- Governments and Nations

- Science and Engineering

- Real Estate

- Travel, Tourism and Hospitality

- Образование

- Startups

- Beauty and Cosmetics

- Agriculture

- Computer Operating Systems

- Crypto

- Politics and News

- Video Review

- Immigration

Больше

Executive Summary Thermic Fluids Market Size and Share: Global Industry Snapshot CAGR Value: The global thermic fluids market size was valued at USD 12.65 billion in 2024 and is expected to reach USD 17.45 billion by 2032, at a CAGR of 4.10% during the forecast period. For an actionable market insight and lucrative business strategies, a...

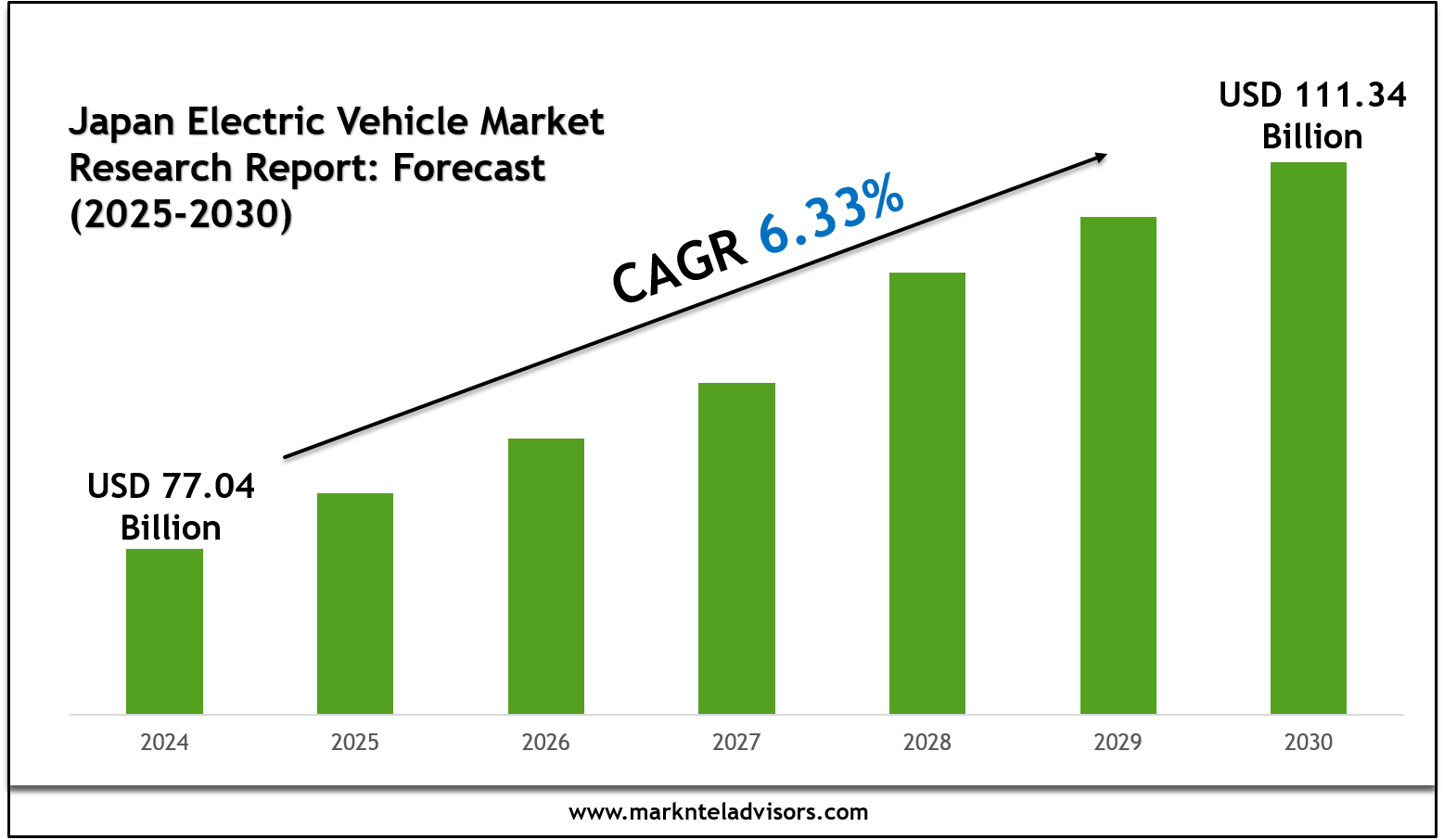

The Japan Electric Vehicle Market reports delivers an in-depth assessment of market size, share, and emerging trends, offering valuable insights into growth opportunities. It examines market segmentation and definitions, highlighting core components and key drivers of expansion. By applying SWOT and PESTEL analyses, the study evaluates the sector’s strengths, weaknesses,...

Competitive Analysis of Executive Summary Liquid Lecithin Market Size and Share CAGR Value: The global liquid lecithin market size was valued at USD 479.56 million in 2024 and is expected to reach USD 817.84 million by 2032, at a CAGR of 6.90% during the forecast period. To stand apart from the competition, a careful idea about the...

The bulk bag dischargers market size was valued at USD 221.80 million in 2024 and is projected to reach USD 285.26 million by 2032, with a CAGR of 3.20% during the forecast period of 2025 to 2032. The global business landscape is undergoing a transformation, with industries increasingly leaning on deep research and actionable insights to make strategic decisions. One segment seeing tremendous...

Executive Summary Methylene Chloride Market Trends: Share, Size, and Future Forecast Data Bridge Market Research analyses that the methylene chloride market was valued at USD 1,453.76 million in 2021 and is expected to reach an estimated value of 1869.55 million in 2029 with a CAGR of 5.2% during the forecast period. The Methylene Chloride Market report provides current as well...