Nylon Industrial Filament Market, Global Outlook and Forecast 2025-2032

The global Nylon Industrial Filament market was valued at US$ 2.3 billion in 2022 and is projected to reach US$ 3.8 billion by 2029, exhibiting a steady CAGR of 6.4% during the forecast period. This growth trajectory underscores the material's expanding role across multiple industrial applications where durability and performance are non-negotiable.

Nylon Industrial Filament represents a specialized category of synthetic fibers engineered for extreme tensile strength and industrial endurance. These high-performance filaments - whether in monofilament or multifilament configurations - are chemically modified to withstand demanding environments that standard fibers cannot. Their unique molecular structure with repeating amide linkages allows for customizable properties through additives, making them indispensable in applications ranging from tire reinforcement to industrial 3D printing.

Get Full Report Here: https://www.24chemicalresearch.com/reports/229882/global-nylon-industrial-filament-forecast-market-2023-2029-97

Market Dynamics:

The Nylon Industrial Filament market is experiencing transformative growth shaped by technological advancements in material science and shifting industrial requirements. While the market shows robust expansion potential, it must simultaneously navigate complex supply chain dynamics and environmental considerations that reshape the competitive landscape.

Powerful Market Drivers Propelling Expansion

-

Tire Industry Reinvention: The automotive sector's shift toward high-performance and eco-friendly tires has created unprecedented demand for nylon reinforcement filaments. These materials improve tire lifespan by 20-25% while reducing rolling resistance by up to 15%, directly impacting fuel efficiency. With global tire production exceeding 2 billion units annually, the market for nylon filament reinforcement is projected to grow at 7.2% annually.

-

Additive Manufacturing Breakthroughs: Industrial 3D printing adoption has surged by 300% since 2018, with nylon filaments capturing over 40% of the polymer filament market. The material's exceptional layer adhesion and thermal stability make it ideal for functional prototypes and end-use parts in aerospace and automotive applications. Recent advances in carbon fiber-infused nylon filaments have elevated temperature resistance to 180°C, opening new possibilities in under-hood automotive components.

-

Marine and Offshore Applications: The marine industry's need for corrosion-resistant materials has led to widespread adoption of specialized nylon filaments for ropes, nets, and mooring lines. These advanced fibers maintain 90% of their tensile strength in saltwater environments, outperforming traditional materials by 3-5x in lifespan. The offshore wind energy sector alone is expected to require 45,000 tons of high-performance nylon filaments annually by 2025.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/229882/global-nylon-industrial-filament-forecast-market-2023-2029-97

Significant Market Restraints Challenging Adoption

Despite its advantages, the market faces obstacles that require strategic solutions for sustained growth.

-

Raw Material Volatility: Cyclohexane and adipic acid prices have shown 18-22% annual volatility, directly impacting nylon filament production costs. This fluctuation creates pricing uncertainty for OEMs and has led to 15-20% margin compression for mid-sized filament producers over the past three years.

-

Recycling Infrastructure Gaps: While nylon is theoretically recyclable, fewer than 30% of industrial facilities currently have the capability to process post-industrial nylon waste. This limitation creates both environmental concerns and missed opportunities for cost-efficient circular manufacturing models.

Critical Market Challenges Requiring Innovation

The industry faces complex technical challenges that demand collaborative solutions:

-

Processing Complexity: Achieving consistent filament diameters below 50 microns - increasingly demanded for precision applications - remains challenging, with current production yields averaging 65-70%. The additional processing steps required to achieve these tolerances add 12-15% to production costs.

-

Thermal Stability Trade-offs: While manufacturers have successfully elevated nylon's heat deflection temperature through additives, these modifications often reduce tensile strength by 10-15%. Finding formulations that optimize both properties remains an ongoing R&D challenge.

Vast Market Opportunities on the Horizon

-

Smart Textile Integration: The emergence of conductive nylon filaments embedded with graphene or metallic nanoparticles opens a $420 million opportunity in industrial sensor textiles. These materials can simultaneously provide structural reinforcement and real-time strain monitoring for critical infrastructure.

-

Hybrid Composite Development: Combining nylon filaments with carbon fiber and thermoplastic matrices creates next-generation composites with 40% higher specific strength than aluminum. The aerospace sector alone could absorb 25,000 tons annually of these advanced materials by 2027.

-

Circular Economy Models: Chemical recycling technologies capable of depolymerizing nylon waste back to caprolactam are achieving 85% efficiency rates. Implementing these processes at scale could reduce filament production costs by 18-22% while addressing environmental concerns.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Nylon 6 and Nylon 6,6, with emerging specialty formulations gaining traction. Nylon 6,6 dominates industrial applications due to its superior thermal stability and mechanical properties, particularly in automotive and electronics applications where temperatures exceed 150°C. However, Nylon 6 maintains strong demand in cost-sensitive applications such as brush bristles and general-purpose industrial textiles.

By Form:

Multifilament configurations lead the market, preferred for their flexibility and strength in woven applications like conveyor belts and hoses. Monofilament variants are seeing accelerated growth in medical applications and precision sieves where dimensional stability is paramount.

By Application:

The automotive and tire industries constitute the largest application segment, accounting for 38% of demand. However, additive manufacturing applications are projected to grow at 9.2% CAGR through 2029 as industrial 3D printing becomes mainstream, particularly in aerospace component production.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/229882/global-nylon-industrial-filament-forecast-market-2023-2029-97

Competitive Landscape:

The global Nylon Industrial Filament market features a mix of chemical conglomerates and specialized manufacturers, with the top five players controlling approximately 42% of market share. DuPont de Nemours, BASF SE, and Ascend Performance Materials lead the sector through vertical integration and strong R&D capabilities, while regional players like Nylstar SA dominate niche European markets.

List of Key Nylon Industrial Filament Companies Profiled:

-

DuPont de Nemours, Inc (U.S.)

-

BASF SE (Germany)

-

Ultimaker BV (Netherlands)

-

Nylstar SA (Spain)

-

Ascend Performance Materials (U.S.)

-

Reliance Industries Limited (India)

-

3DGence (Poland)

-

Keene Village Plastics (U.S.)

-

Taulman3D, LLC (U.S.)

-

LeaLea Group (Taiwan)

Competitive strategies are increasingly focused on sustainable production methods, with leading companies investing 8-12% of revenues in bio-based nylon development and recycling technologies. Partnerships with end-users for application-specific filament development have become critical to maintaining market position.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Commands 48% of global consumption, driven by China's massive industrial base and growing automotive production. The region's filament producers are aggressively expanding high-value specialty nylon capacity to reduce reliance on imports.

-

North America: The mature but innovation-driven North American market excels in high-performance nylon filament production, particularly for aerospace and defense applications. Local manufacturers maintain technological leadership through extensive R&D collaborations with academic institutions.

-

Europe: Strict environmental regulations have positioned European producers as sustainability leaders, with 35% of regional production now using recycled or bio-based inputs. The region maintains particular strength in industrial textile applications.

Get Full Report Here: https://www.24chemicalresearch.com/reports/229882/global-nylon-industrial-filament-forecast-market-2023-2029-97

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/229882/global-nylon-industrial-filament-forecast-market-2023-2029-97

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Patrocinado

Patrocinado

Categorias

- AI

- Design

- Fashion and Art

- Investment and Finance

- Top 10

- Christianity

- Climate and Enviroment

- Writing and Film

- Fitness

- Food

- Jogos

- Gardening

- Health

- Home and Interiors

- Marketing and Sales

- Music

- Making Money Online

- Others

- Books

- Religion

- Ecommerce

- Sports

- Cars

- Wellness

- Tech Gadgets

- Eventos

- Governments and Nations

- Science and Engineering

- Real Estate

- Travel, Tourism and Hospitality

- Educação

- Startups

- Beauty and Cosmetics

- Agriculture

- Computer Operating Systems

- Crypto

- Politics and News

- Video Review

- Immigration

Leia Mais

The global Cargo Bike market is witnessing rapid growth as cities and businesses increasingly prioritize sustainable and efficient urban logistics solutions. Market Intelo unveils a detailed analysis of the cargo bike sector, which belongs to the Automotive & Logistics parent category and the On-Highway & Off-Highway Vehicles child category, highlighting key trends, growth drivers, and...

Regional Overview of Executive Summary Pyogenic Arthritis, Pyoderma Gangrenosum and Acne (PAPA) Syndrome Treatment Market by Size and Share Pyogenic arthritis, pyoderma gangrenosum and acne (PAPA) syndrome treatment market is expected to gain market growth in the forecast period of 2022-2029. Data Bridge Market Research analyses the market to account to grow at a CAGR of 4.70% in the...

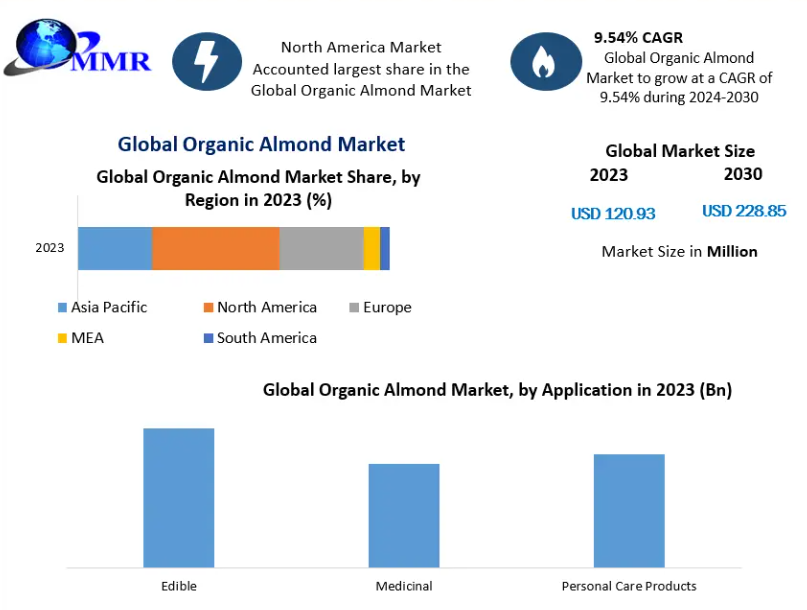

Market Overview The Organic Almond Market is growing steadily due to increasing health awareness and rising consumer preference for organic foods. Almonds are nutrient-dense, providing proteins, vitamins, minerals, antioxidants, and healthy fats. Organic almonds are cultivated without synthetic pesticides and chemicals, making them safer for regular consumption. They are sourced from...

The global Wollastonite Powder Market is poised for substantial growth, driven by its unique performance attributes as a non-toxic, acicular mineral filler and additive across key industrial sectors. The wollastonite powder market is estimated to grow at a compound annual growth rate of 8.60% for the forecast period of 2021 to 2028. The market is projected to reach an...

According to a new report from Intel Market Research, the global PFAS Free Barrier Coating market was valued at US$ 1,312 million in 2024 and is projected to reach US$ 1,776 million by 2032, growing at a steady CAGR of 5.0% during the forecast period (2025–2032). This growth trajectory aligns with increasing regulatory pressures on PFAS chemicals and accelerating demand for...