Polymer Emulsions Market, Global Outlook and Forecast 2025-2032

Global Polymer Emulsions market was valued at USD 33 billion in 2024 and is projected to reach USD 46.66 billion by 2032, exhibiting a steady CAGR of 5.2% during the forecast period.

Polymer emulsions, the water-based dispersions of polymeric particles, have become essential across multiple industries due to their environmentally friendly nature and superior performance characteristics. These colloidal systems offer critical advantages over solvent-borne alternatives, including lower VOC emissions, easier clean-up, and improved safety profiles. From architectural coatings to advanced adhesives, polymer emulsions enable the development of high-performance products that meet increasingly stringent environmental regulations while maintaining exceptional quality standards. The shift toward sustainable manufacturing practices has positioned this technology as a cornerstone of modern material science.

Get Full Report Here: https://www.24chemicalresearch.com/reports/297883/global-polymer-emulsions-forecast-market-2025-2032-478

Market Dynamics:

The polymer emulsions market operates within a complex ecosystem of technological innovation, regulatory pressures, and shifting industry demands that collectively shape its growth trajectory. Understanding these multifaceted dynamics provides critical insight into both current conditions and future opportunities.

Powerful Market Drivers Propelling Expansion

-

Construction Boom and Architectural Coatings Demand: The global construction sector's expansion, particularly in emerging economies, represents the single most significant growth driver for polymer emulsions. With construction output projected to reach $15.5 trillion by 2030, the demand for high-performance water-based coatings and adhesives continues to surge. Cities across Asia are witnessing unprecedented urbanization rates, with China and India alone accounting for nearly 40% of global construction activity. Architectural coatings incorporating acrylic emulsions now dominate the market due to their durability, washability, and environmental compliance – crucial factors in green building certifications.

-

Regulatory Shift Toward Sustainable Materials: The regulatory landscape has become a powerful accelerant for polymer emulsion adoption. Global initiatives like the EU's REACH legislation and the U.S. EPA's VOC limits have dramatically altered industry preferences. Recent standards mandating VOC content below 50 g/L in architectural coatings have made water-based systems particularly attractive. Furthermore, sustainability commitments from major manufacturers are driving R&D investments in bio-based emulsion technologies. The paints and coatings sector, consuming approximately 45% of polymer emulsions, exemplifies this transition as formulators replace traditional solvent-borne systems.

-

Automotive and Industrial Coating Innovations: The industrial coatings segment is undergoing a quiet revolution through emulsion technology. Modern automotive OEM coatings increasingly utilize acrylic and polyurethane hybrid emulsions that deliver comparable performance to solvent-based systems while meeting stringent environmental standards. These formulations achieve remarkable improvements in chip resistance (up to 30% better than previous generations) and weathering performance, enabling thinner, more efficient coating layers. Industrial maintenance coatings based on vinyl acetate ethylene (VAE) emulsions demonstrate similar advances, offering corrosion protection that extends asset lifetimes by 5-7 years.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/297883/global-polymer-emulsions-forecast-market-2025-2032-478

Significant Market Restraints Challenging Adoption

While the market demonstrates strong growth potential, several obstacles must be addressed to achieve widespread penetration across all potential applications.

-

Raw Material Volatility and Supply Chain Constraints: The polymer emulsions industry faces ongoing challenges from fluctuating raw material costs. Key monomers like styrene and acrylic acid have experienced price swings of 15-25% annually, significantly impacting production economics. Supply chain disruptions have exacerbated this situation, with regional production capacities struggling to meet global demand. For emulsion manufacturers, maintaining consistent quality while managing input cost fluctuations remains an ongoing operational challenge, particularly for smaller producers lacking scale advantages.

-

Performance Limitations in Specialty Applications: Despite significant formulation advancements, water-based emulsions still face technical barriers in certain demanding applications. High-temperature industrial environments, chemical processing equipment, and specialty adhesives continue to favor solvent-borne systems due to their superior chemical resistance and faster drying characteristics. The performance gap, while narrowing, remains a substantial hurdle in price-insensitive segments where technical requirements outweigh environmental considerations.

Critical Market Challenges Requiring Innovation

The transition from laboratory innovation to industrial-scale production presents its own set of complex challenges. Many emulsion manufacturers struggle with batch-to-batch consistency when scaling up production, with yield losses sometimes reaching 10-15% during process optimization. Achieving stable viscosity and particle size distribution becomes increasingly difficult at commercial volumes, requiring sophisticated process control systems. Furthermore, maintaining emulsion stability during transportation and storage, especially in variable climate conditions, continues to test formulation scientists.

Simultaneously, the industry faces growing pressure to reduce its carbon footprint. Polymer emulsion manufacturing remains energy-intensive, particularly during the temperature-controlled polymerization phase. While some producers have implemented energy recovery systems, most facilities still require substantial process innovations to meet ambitious sustainability targets. The competitive landscape amplifies these challenges as companies balance R&D investments against margin pressures in an increasingly cost-conscious market.

Vast Market Opportunities on the Horizon

-

Renewable Energy Sector Expansion: The booming renewable energy industry presents exceptional growth potential for specialty polymer emulsions. Wind turbine blade coatings using advanced acrylic-styrene emulsions demonstrate 25-30% better weather resistance than conventional systems. Solar panel encapsulation adhesives based on low-yellowing emulsions are gaining traction in the photovoltaic sector, which is projected to grow at 8% annually through 2030. These applications demand specialized formulations that combine durability with environmental resistance—precisely the sweet spot for next-generation emulsions.

-

Bio-based Emulsion Breakthroughs: Sustainable emulsion technologies are reaching critical commercial viability. Formulations incorporating plant-derived monomers now account for nearly 15% of new product development pipelines. Recent advancements in bio-acrylics demonstrate performance parity with petroleum-based counterparts while reducing carbon footprints by 40-50%. The packaging industry, particularly food-contact applications, shows strong interest in these developments as brand owners seek environmentally responsible solutions without compromising performance.

-

Emerging Market Infrastructure Development: Developing economies represent the next frontier for polymer emulsion adoption. Countries across Southeast Asia, Africa, and Latin America are investing heavily in infrastructure while implementing environmental regulations modeled after developed markets. The polymer emulsions market in these regions grows at nearly double the global average, with particular strength in architectural coatings and paper coatings. Companies establishing local production and technical support capabilities stand to gain first-mover advantages in these high-growth territories.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Acrylics, Vinyl Acetate Polymers, SB Latex, Polyurethane Dispersions, and Others. Acrylic emulsions dominate the landscape, capturing over 40% market share due to their exceptional versatility across coatings, adhesives, and construction applications. These water-based systems offer superior UV resistance and durability—critical properties for exterior applications. Styrene-butadiene latex follows closely, preferred in paper coating and carpet backing applications where its flexibility and adhesion properties excel.

By Application:

Application segments include Paints & Coatings, Adhesives & Sealants, Paper & Paperboard, Textiles & Non-Wovens, and Others. The Paints & Coatings segment maintains clear dominance, accounting for nearly half of global demand. This reflects both the construction industry's massive scale and ongoing conversions from solvent-based systems. The adhesives sector shows particularly strong growth potential with innovations in pressure-sensitive and structural bonding applications driving adoption.

By Technology:

Within technological approaches, water-based systems represent the clear preference, holding over 70% market share by volume. Their environmental advantages and regulatory compliance drive consistent growth across all regions. Hybrid technologies combining water-based and reactive chemistries are emerging as an important niche, particularly in industrial coating applications where performance requirements push the boundaries of conventional emulsion capabilities.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/297883/global-polymer-emulsions-forecast-market-2025-2032-478

Competitive Landscape:

The global polymer emulsions market features a mix of multinational chemical giants and specialized producers competing across technology and application segments. BASF, Dow, and Trinseo collectively command approximately 33% market share, leveraging their integrated raw material positions and extensive R&D capabilities. These industry leaders continue to drive innovation through substantial investments in bio-based technologies and application-specific solutions.

European producers like Wacker Chemie and Synthomer maintain strong positions in vinyl-based emulsions and specialty adhesives, while Asian manufacturers such as DIC Corporation compete effectively in regional markets through cost-optimized production. The competitive environment remains dynamic as companies balance portfolio diversification with technical specialization to address evolving market needs.

List of Key Polymer Emulsions Companies Profiled:

-

BASF SE (Germany)

-

Dow Chemical Company (U.S.)

-

Trinseo (Styron) (U.S.)

-

AkzoNobel (Netherlands)

-

Wacker Chemie AG (Germany)

-

Celanese Corporation (U.S.)

-

Arkema SA (France)

-

Clariant AG (Switzerland)

-

Hexion Inc. (U.S.)

-

Synthomer plc (UK)

-

DIC Corporation (Japan)

-

Dairen Chemical Corporation (Taiwan)

Competitive strategies increasingly emphasize sustainability, with leading players investing heavily in green chemistry initiatives. Vertical integration remains important for cost control, while strategic partnerships with end-users foster application-specific innovation. The market continues to consolidate as companies seek to bolster their technical capabilities and geographic reach through targeted acquisitions.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Europe: Leads global consumption with a 29% market share, driven by stringent environmental regulations and advanced manufacturing capabilities. Germany and France represent the largest national markets, supported by robust automotive and construction sectors. The region remains at the forefront of sustainable emulsion development, with bio-based formulations gaining significant traction.

-

North America: Accounts for approximately 22% of global demand, with the U.S. dominating regional consumption. Strong regulatory standards and a thriving construction sector support steady growth. The region demonstrates particular strength in high-performance industrial coatings and specialty adhesives applications.

-

Asia-Pacific: Emerging as the fastest-growing regional market, fueled by rapid industrialization and urbanization. China leads regional expansion with extensive infrastructure investments, while Southeast Asian nations show accelerating adoption rates. Local producers are gaining market share through cost-competitive offerings tailored to regional needs.

Get Full Report Here: https://www.24chemicalresearch.com/reports/297883/global-polymer-emulsions-forecast-market-2025-2032-478

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/297883/global-polymer-emulsions-forecast-market-2025-2032-478

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Patrocinado

Patrocinado

Categorias

- AI

- Design

- Fashion and Art

- Investment and Finance

- Top 10

- Christianity

- Climate and Enviroment

- Writing and Film

- Fitness

- Food

- Jogos

- Gardening

- Health

- Home and Interiors

- Marketing and Sales

- Music

- Making Money Online

- Others

- Books

- Religion

- Ecommerce

- Sports

- Cars

- Wellness

- Tech Gadgets

- Eventos

- Governments and Nations

- Science and Engineering

- Real Estate

- Travel, Tourism and Hospitality

- Educação

- Startups

- Beauty and Cosmetics

- Agriculture

- Computer Operating Systems

- Crypto

- Politics and News

- Video Review

- Immigration

Leia mais

The global Natural Delta Dodecalactone market demonstrates steady expansion, with a valuation reaching US$ 67 million in 2024. Industry projections indicate a compound annual growth rate (CAGR) of 5.0% through 2032, potentially achieving US$ 95 million by the forecast period's end. This organic lactone compound, prized for its peach-like aroma and flavor-enhancing...

Latest Insights on Executive Summary North America Adhesive Tapes Market Share and Size Data Bridge Market Research analyses the North America adhesive tapes market will exhibit a CAGR of 5.62 for the forecast period of 2022-2029. This North America Adhesive Tapes Market research report proves to be true in serving the purpose of businesses of making enhanced decisions, deal with...

Executive Summary Modified Atmosphere Packaging Market Opportunities by Size and Share The global modified atmosphere packaging market size was valued at USD 15.74 billion in 2024 and is expected to reach USD 20.57 billion by 2032, at a CAGR of 3.40% during the forecast period Modified Atmosphere Packaging Market research report is a verified and consistent source...

Key Drivers Impacting Executive Summary Veterinary-Animal Vaccines Market Size and Share CAGR Value: Data Bridge Market Research analyses that the veterinary-animal vaccines market, which was USD 10.69 billion in 2022, would rise to USD 18.23 billion by 2030 and is expected to undergo a CAGR of 6.9% during the forecast period from 2023 to 2030. Analysis and discussion of...

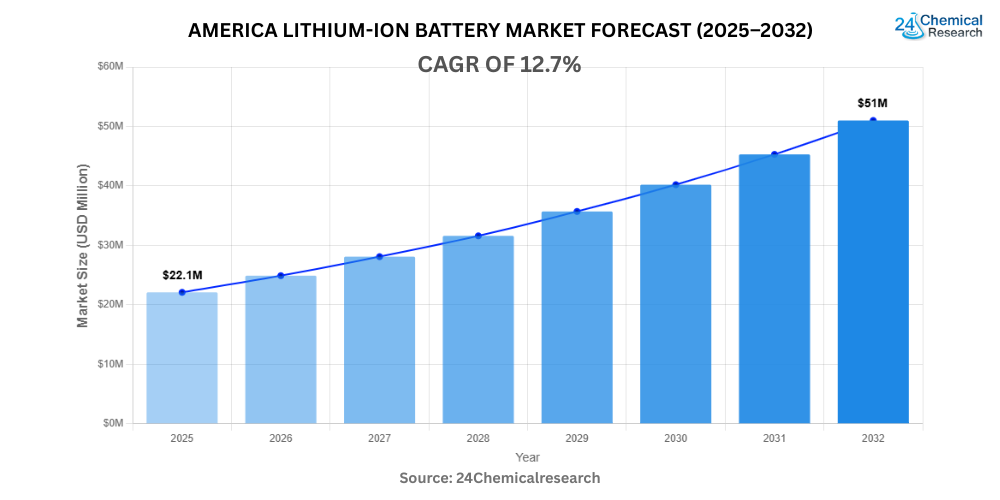

North America lithium-ion battery market was valued at USD 22.1 billion in 2024. The market is projected to grow from USD 26.4 billion in 2025 to USD 68.9 billion by 2032, exhibiting a CAGR of 12.7% during the forecast period. Lithium-ion batteries have become the backbone of modern energy systems, powering everything from smartphones to electric vehicles (EVs) and grid-scale storage. Their...