Diabetes Drugs Market to Reach USD 198.73 Billion by 2032, Growing at 12.1% CAGR

MARKET INSIGHTS

Global diabetes drugs market was valued at US$ 88.96 billion in 2025 and is projected to reach US$ 198.73 billion by 2032, exhibiting a CAGR of 12.1% during the forecast period.

Get FREE Sample of this Report at https://www.intelmarketresearch.com/download-free-sample/15749/diabetes-drugs-market

Diabetes drugs are treatments for diabetes by lowering the sugar in the blood. Diabetes is a kind of disease with common symptoms such as frequent urination, increased thirst and weight loss. The most common drugs used are insulin and oral medications.

Global Diabetes Drugs key players include Novo Nordisk, Sanofi, Eli Lilly, Merck & Co, Boehringer Ingelheim, and others. The top five manufacturers globally hold a share over 62%. In terms of product type, Injection is the largest segment, with a share of 60%. By application, the Hospital segment holds a share of about 67%.

The market is experiencing rapid growth due to several factors, including the increasing global prevalence of diabetes, particularly type 2 diabetes, driven by sedentary lifestyles and unhealthy diets. Additionally, the growing geriatric population, which is more susceptible to diabetes, contributes to market expansion. Furthermore, advancements in drug delivery systems, such as the development of more convenient and effective insulin pens and pumps, are encouraging better patient compliance. Strategic initiatives by key players, including mergers, acquisitions, and the launch of new products with improved efficacy and safety profiles, are also expected to fuel market growth. For instance, in January 2024, Eli Lilly received FDA approval for its once-weekly GLP-1 drug, tirzepatide, which has shown significant efficacy in clinical trials.

Rising Global Prevalence of Diabetes

The diabetes drugs market is primarily driven by the escalating global prevalence of diabetes mellitus, particularly type 2 diabetes. The increasing incidence is strongly linked to aging populations, sedentary lifestyles, and the growing obesity epidemic. The International Diabetes Federation reports hundreds of millions of people are living with diabetes worldwide, creating a substantial and continuously expanding patient pool requiring lifelong management and medication.

Advances in Drug Development and Innovation

Significant pharmaceutical innovation is a major driver. The shift from traditional therapies like insulin and metformin to newer classes, such as GLP-1 receptor agonists and SGLT2 inhibitors, has transformed treatment paradigms. These drugs offer improved efficacy, better glucose control, weight loss benefits, and demonstrated cardiovascular and renal protective effects, increasing their adoption by healthcare providers.

➤ Technological integration, including connected devices and smart insulin pens, is enhancing drug delivery and patient adherence, further propelling market growth.

The supportive regulatory environment with expedited approval pathways for novel therapies and the expansion of healthcare access in emerging economies are also crucial drivers ensuring these advanced treatments reach a broader patient base.

MARKET CHALLENGES

High Treatment Costs and Pricing Pressures

A primary challenge is the high cost of newer, advanced diabetes drugs, which can limit patient access, especially in cost-sensitive markets and for underinsured populations. Healthcare systems and payers are imposing stringent cost-containment measures and demanding robust evidence of cost-effectiveness, creating pricing pressure for manufacturers.

Other Challenges

Intense Market Competition and Patent Expiries

The market is highly competitive with numerous established and emerging players. The expiration of patents for blockbuster drugs leads to the entry of biosimilars and generics, eroding the revenues of originator companies and intensifying price competition, which can impact profitability and innovation funding.

Complex Regulatory Hurdles and Safety Concerns

Navigating the complex and varying regulatory requirements across different regions is challenging and time-consuming. Furthermore, ensuring the long-term safety profile of new drug classes remains paramount, as any emerging adverse effects can lead to stringent labeling restrictions or market withdrawals.

Stringent Regulatory Approval Processes

The rigorous and lengthy regulatory approval process for new diabetes drugs acts as a significant market restraint. Regulatory agencies require extensive clinical trial data demonstrating not only efficacy but also cardiovascular safety, which increases development time and costs considerably, potentially delaying market entry for new therapies.

Growing Preference for Non-Pharmacological Interventions

There is a growing emphasis on lifestyle modifications, including diet and exercise, as first-line interventions for managing type 2 diabetes, particularly in its early stages. This trend, promoted by public health initiatives, can delay the initiation of drug therapy, temporarily restraining market growth for pharmaceutical interventions.

Expansion in Emerging Markets

Rapidly developing economies in Asia Pacific, Latin America, and the Middle East present significant growth opportunities. Increasing diagnostic rates, improving healthcare infrastructure, rising disposable incomes, and growing health insurance penetration are expanding the addressable patient base for diabetes drugs in these regions.

Development of Combination Therapies and Personalized Medicine

There is a substantial opportunity in the development of fixed-dose combination drugs that improve patient compliance by reducing pill burden. Furthermore, advances in personalized medicine, leveraging genetic and biomarker research to tailor treatments to individual patient profiles, are opening new avenues for targeted and more effective therapies.

Focus on Weight Management and Comorbidity Benefits

The proven weight-loss benefits of GLP-1 agonists and the cardiovascular and renal protection offered by SGLT2 inhibitors allow these drugs to be positioned beyond glucose control. This expansion into treating common comorbidities creates new revenue streams and strengthens their value proposition in the market.

Get the Complete Report & TOC at https://www.intelmarketresearch.com/pharmaceuticals/15749/diabetes-drugs-market

Segment Analysis:

Segment CategorySub-SegmentsKey InsightsBy Type

-

Injection

-

Oral

Injection is the dominant modality in the diabetes drugs market, primarily driven by the critical and widespread use of various insulin formulations for managing blood glucose levels. This segment’s preeminence is sustained by the large and growing population of patients with Type 1 diabetes, whose survival depends on exogenous insulin, as well as the increasing number of advanced-stage Type 2 diabetes patients requiring intensive insulin therapy. The introduction of advanced long-acting and ultra-fast-acting insulin analogs has further solidified this segment’s leading position, offering patients greater flexibility and improved glycemic control. Continuous innovation in delivery devices, such as insulin pens and smart pumps, enhances patient convenience and adherence, underpinning the sustained dominance of injectable treatments despite the convenience offered by oral alternatives.By Application

-

Hospital

-

Retail Pharmacy

-

Online Pharmacy

-

Others

Hospital pharmacies represent the leading channel for diabetes drug distribution, largely due to the management of complex diabetic cases and acute complications requiring hospitalization. This channel is critical for initiating new, often injectable, therapies under medical supervision, especially for patients with severe hyperglycemia or those experiencing diabetic emergencies. Hospitals serve as a primary point of care for diagnosis, treatment initiation, and management of co-morbidities associated with diabetes, ensuring a consistent demand for a wide range of medications. Furthermore, the procurement of specialized and high-cost biologics, coupled with the need for patient education on dosage and administration, firmly establishes hospitals as the central hub for diabetes care, driving their leading position in the application segment.By End User

-

Type 1 Diabetes Patients

-

Type 2 Diabetes Patients

-

Gestational Diabetes Patients

Type 2 Diabetes Patients constitute the largest and fastest-growing end-user segment, a direct consequence of the global epidemic of obesity and sedentary lifestyles. The immense patient pool, driven by rising prevalence rates across all age groups and geographies, creates a sustained and expanding demand for a diverse array of therapeutic agents, from first-line metformin to newer classes like SGLT2 inhibitors and GLP-1 receptor agonists. The progression of the disease often necessitates treatment intensification over time, leading to long-term medication use and creating a robust, recurring market. This demographic’s size and the chronic nature of the condition ensure that Type 2 diabetes remains the primary driver of market volume and innovation, with drug development heavily focused on addressing its specific pathophysiological pathways and associated cardiovascular risks.By Drug Class

-

Insulin

-

Biguanides

-

GLP-1 Receptor Agonists

-

SGLT2 Inhibitors

-

Others

Insulin remains the cornerstone therapeutic class, holding a foundational and dominant role in diabetes management. Its irreplaceable nature for Type 1 diabetes patients and critical use in advanced Type 2 diabetes ensures its consistent and high-volume utilization. The segment is characterized by continuous innovation, with the development of next-generation analogs offering improved pharmacokinetic profiles that mimic physiological insulin secretion more closely, thereby reducing the risk of hypoglycemia. Furthermore, the high brand loyalty and complex manufacturing processes create significant barriers to entry, allowing established players to maintain strong market positions. The essential life-sustaining nature of insulin therapy, combined with ongoing demographic and epidemiological trends, secures its leadership position within the drug class segmentation.By Distribution Model

-

Prescription-Based

-

Over-the-Counter

Prescription-Based distribution is the unequivocal leader, as the vast majority of diabetes medications, particularly insulin and newer antidiabetic agents, are potent pharmaceuticals requiring strict medical supervision and dosing individualization. This model is mandated by regulatory authorities worldwide to ensure patient safety, given the risks of hypoglycemia and other serious side effects associated with improper use. The management of diabetes is a continuous process involving regular physician consultations for monitoring and treatment adjustments, which naturally ties drug acquisition to prescription renewals. The complexity of treatment regimens and the critical need for adherence to clinical guidelines reinforce the dominance of the prescription-based channel, making it the primary conduit for accessing effective and safe diabetes care.

COMPETITIVE LANDSCAPE

A Market Dominated by a Few Major Innovators

The global diabetes drugs market is characterized by a high degree of consolidation, with the top five manufacturers collectively commanding a significant portion of the market share. Industry leader Novo Nordisk maintains a prominent position, largely driven by its extensive portfolio of both modern and human insulins, along with GLP-1 receptor agonists. Sanofi and Eli Lilly and Company are other key global giants, forming a triumvirate that dominates the insulin segment. This concentration of market power is reinforced by substantial investments in research and development, extensive global distribution networks, and strong brand recognition. The competitive dynamics are heavily influenced by the ongoing transition from older therapies to newer, more effective drug classes and the intense competition in the biosimilars space, particularly for insulin products.

Beyond the dominant players, a number of other significant companies compete effectively in specific niches or regions. Pharmaceutical powerhouses like Merck & Co., AstraZeneca, and Boehringer Ingelheim have strong positions with their oral antidiabetic medications, including SGLT2 inhibitors and DPP-4 inhibitors. Johnson & Johnson, through its subsidiary Janssen Pharmaceuticals, is also a notable contender. The market also features important regional players, such as China’s Tonghua Dongbao, which is a major supplier of recombinant human insulin in the Asia-Pacific region. Companies like Biocon are playing an increasingly important role in the development and commercialization of biosimilar insulins, increasing competition and accessibility.

List of Key Diabetes Drugs Companies Profiled

-

Novo Nordisk

-

Merck & Co.

-

Bayer AG

-

Boehringer Ingelheim

-

Johnson & Johnson (Janssen Pharmaceuticals)

-

Takeda Pharmaceutical Company

-

Tonghua Dongbao

-

United Pharmaceuticals

-

Novartis

-

Wockhardt

Get the Complete Report & TOC at https://www.intelmarketresearch.com/pharmaceuticals/15749/diabetes-drugs-market

Diabetes Drugs Market Trends

Market Expansion Driven by Rising Global Prevalence

The global Diabetes Drugs market is on a significant growth trajectory, reflecting the increasing worldwide burden of diabetes. Valued at $88,960 million in 2025, the market is projected to expand to $198,730 million by 2032, achieving a robust compound annual growth rate of 12.1%. This sustained growth is primarily fueled by the rising global prevalence of diabetes, a chronic condition characterized by symptoms like frequent urination and increased thirst. The market’s expansion is supported by continuous pharmaceutical innovation and an increasing focus on effective glycemic control to manage the disease and its complications.

Other Trends

Dominance of Injection-Based Treatments and Hospital Distribution

The market is heavily segmented by product type and application, with clear leaders in both categories. Injection-based drugs, primarily insulin, dominate the product landscape, holding a substantial 60% market share due to their efficacy in managing blood sugar levels. Oral medications represent the other key segment. In terms of application, the hospital channel is the primary distribution pathway, accounting for approximately 67% of the market, underscoring the critical role of clinical settings in the administration and management of these treatments, particularly for more complex cases.

Consolidated Competitive Landscape and Regional Dynamics

The competitive environment is characterized by a high degree of consolidation, with the top five manufacturers including Novo Nordisk, Sanofi, and Eli Lilly collectively holding over 62% of the global market share. This concentration highlights the significant barriers to entry and the importance of scale in research, development, and distribution. Geographically, the market spans North America, Europe, Asia, South America, and the Middle East & Africa. Asia is a key region for future growth, driven by large patient populations, increasing healthcare expenditure, and growing awareness. Market dynamics are influenced by factors such as pricing pressures, the introduction of biosimilars, regulatory changes, and the ongoing pursuit of next-generation therapies with improved efficacy and convenience.

Regional Analysis: Diabetes Drugs Market

North America

North America firmly holds the leading position in the global diabetes drugs market, driven by a powerful combination of a high disease prevalence, particularly of type 2 diabetes, and a mature, technologically advanced healthcare infrastructure. The region is characterized by high patient awareness, robust diagnostic rates, and a strong emphasis on chronic disease management, creating consistent demand for both established and novel therapeutics. High healthcare expenditure, comprehensive insurance coverage for many patients, and favorable reimbursement policies for advanced treatments, including newer drug classes like GLP-1 receptor agonists and SGLT2 inhibitors, significantly boost market access and penetration. The presence of major global pharmaceutical companies headquartered in the region, combined with a rigorous yet supportive regulatory environment from the U.S. Food and Drug Administration (FDA), accelerates drug development and approval timelines. Furthermore, a well-established network of specialists and primary care physicians ensures widespread adoption of updated treatment guidelines, promoting the use of effective combination therapies. The market is also heavily influenced by intense competition and strategic marketing efforts, which drive continuous innovation and product differentiation.

Advanced Healthcare Infrastructure

The sophisticated healthcare system in North America facilitates excellent patient access to diagnostics and specialist care. This infrastructure supports the early detection of diabetes and the subsequent long-term management with appropriate drug regimens. Hospitals, clinics, and pharmacy networks are well-integrated, ensuring a continuous supply chain for essential medications and patient adherence support programs.

Favorable Reimbursement Landscape

Reimbursement policies from both public and private payers in the United States and Canada are relatively favorable towards newer, higher-cost diabetes drugs. This reduces the financial burden on patients and encourages physicians to prescribe advanced therapeutic options, thereby driving the uptake of innovative treatments and sustaining high market value.

Strong R&D and Innovation Hub

As home to many leading biopharmaceutical companies and research institutions, North America is a central hub for diabetes drug research and development. This concentration of expertise leads to a pipeline rich with novel mechanisms of action and delivery systems, keeping the region at the forefront of therapeutic advancements and first-in-market launches.

High Patient Awareness and Education

Extensive public health campaigns and educational initiatives by various organizations have resulted in high levels of patient awareness about diabetes management. This educated patient population is more likely to seek treatment, adhere to prescribed drug therapies, and demand newer, more effective options, which in turn stimulates market growth.

Europe

Europe represents a highly significant and mature market for diabetes drugs, characterized by strong universal healthcare systems that provide broad access to treatments. The region benefits from centralized regulatory oversight through the European Medicines Agency (EMA), which standardizes and streamlines drug approvals across member states. There is a strong emphasis on cost-containment and health technology assessments, which influence prescribing patterns and market access for new drugs. Countries like Germany, the UK, and France are major contributors, with well-established guidelines for diabetes care that promote the use of effective therapies. The market faces pressures from generic competition for older drugs, but also shows robust uptake of innovative products that demonstrate clear patient benefits. Cultural and economic diversity across the continent leads to varying adoption rates of new treatments, creating a complex but dynamic market environment.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for diabetes drugs, fueled by a rapidly increasing prevalence of diabetes, particularly in populous countries like China and India. Rising disposable incomes, urbanization, and changing lifestyles are key drivers of this epidemic, creating a vast and expanding patient pool. While the market potential is enormous, access to advanced and expensive drugs can be limited by economic disparities and varying levels of healthcare infrastructure. Price sensitivity is a major factor, with a high volume of generic drug usage. However, local pharmaceutical companies are increasingly developing biosimilars and innovative formulations, making treatment more accessible. Governments are also launching national diabetes control programs, which are gradually improving diagnosis rates and treatment accessibility, signaling strong long-term growth prospects for the market.

South America

The diabetes drugs market in South America is experiencing steady growth, driven by increasing disease prevalence and gradual improvements in healthcare access. Countries like Brazil and Argentina have large patient populations and public healthcare systems that strive to provide essential medicines, though budget constraints can limit the availability of the latest branded drugs. The market is characterized by a mix of multinational and local pharmaceutical companies, with a significant share held by generic medications due to cost considerations. Economic volatility in some countries can impact drug pricing and reimbursement policies, creating a somewhat unpredictable environment. Despite these challenges, there is a growing awareness of diabetes management, and efforts are being made to incorporate newer drug classes into public formularies, pointing towards future market expansion.

Middle East & Africa

The Middle East & Africa region presents a highly diverse and emerging market for diabetes drugs, with significant variations between the oil-rich Gulf Cooperation Council (GCC) nations and other developing countries. The GCC countries have high diabetes prevalence rates and invest heavily in advanced healthcare infrastructure, facilitating access to innovative therapies. In contrast, many African nations face challenges related to limited healthcare funding, infrastructure, and access to essential medicines, leading to a high reliance on international aid and low-cost generics. The entire region is witnessing a rapid rise in diabetes cases, creating urgent unmet medical needs. Market growth is supported by government initiatives to combat non-communicable diseases and increasing private sector investment in healthcare, although the pace of development is uneven across the region.

Get FREE Sample of this Report at https://www.intelmarketresearch.com/download-free-sample/15749/diabetes-drugs-market

Get the Complete Report & TOC at https://www.intelmarketresearch.com/pharmaceuticals/15749/diabetes-drugs-market

Report Scope

This market research report offers a holistic overview of global and regional markets for the forecast period 2025–2032. It presents accurate and actionable insights based on a blend of primary and secondary research.

Key Coverage Areas:

-

✅ Market Overview

-

Global and regional market size (historical & forecast)

-

Growth trends and value/volume projections

-

-

✅ Segmentation Analysis

-

By product type or category

-

By application or usage area

-

By end-user industry

-

By distribution channel (if applicable)

-

-

✅ Regional Insights

-

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

-

Country-level data for key markets

-

-

✅ Competitive Landscape

-

Company profiles and market share analysis

-

Key strategies: M&A, partnerships, expansions

-

Product portfolio and pricing strategies

-

-

✅ Technology & Innovation

-

Emerging technologies and R&D trends

-

Automation, digitalization, sustainability initiatives

-

Impact of AI, IoT, or other disruptors (where applicable)

-

-

✅ Market Dynamics

-

Key drivers supporting market growth

-

Restraints and potential risk factors

-

Supply chain trends and challenges

-

-

✅ Opportunities & Recommendations

-

High-growth segments

-

Investment hotspots

-

Strategic suggestions for stakeholders

-

-

✅ Stakeholder Insights

-

Target audience includes manufacturers, suppliers, distributors, investors, regulators, and policymakers

-

-> Global Diabetes Drugs Market was valued at USD 88,960 million in 2025 and is projected to reach USD 198,730 million by 2032, exhibiting a CAGR of 12.1% during the forecast period.

-> Key players include Novo Nordisk, Sanofi, Eli Lilly, Merck & Co, and Boehringer Ingelheim, with the top five manufacturers holding a combined market share of over 62%.

-> Key growth drivers include the rising global prevalence of diabetes, increasing awareness and diagnosis rates, and continuous advancements in drug formulations such as insulin and oral medications.

-> The report provides detailed analysis for key regions including North America, Europe, Asia, South America, and Middle East & Africa, with country-level data for major markets.

-> The report analyzes key market dynamics, including industry trends, drivers, challenges, obstacles, and potential risks, along with recent developments from manufacturers.

Sponsor

Sponsor

Categorieën

- AI

- Ontwerp

- Fashion and Art

- Investment and Finance

- Top 10

- Christianity

- Climate and Enviroment

- Writing and Film

- Fitness

- Food

- Spellen

- Gardening

- Health

- Home and Interiors

- Marketing and Sales

- Music

- Making Money Online

- Others

- Books

- Religion

- Ecommerce

- Sports

- Cars

- Wellness

- Tech Gadgets

- Events

- Governments and Nations

- Science and Engineering

- Real Estate

- Travel, Tourism and Hospitality

- Onderwijs

- Startups

- Beauty and Cosmetics

- Agriculture

- Computer Operating Systems

- Crypto

- Politics and News

- Video Review

- Immigration

Read More

Comprehensive Outlook on Executive Summary Essential Oil Extraction Market Size and Share CAGR Value: Global essential oil extraction market size was valued at USD 13.36 billion in 2024 and is projected to reach USD 28.65 billion by 2032, with a CAGR of 10.00% during the forecast period of 2025 to 2032. This competitive era calls for businesses to be equipped with knowhow...

Executive Summary Baby Food and Infant Formula Market Opportunities by Size and Share Data Bridge Market Research analyses that the baby food and infant formula market was valued at USD 33.3 billion in 2021 and is expected to reach the value of USD 50.34 billion by 2029, at a CAGR of 5.3% during the forecast period of 2022-2029. Baby Food and Infant Formula Market research report is a...

Electric Noodle Maker offers a seamless way to bring fresh, delicious noodles into both home and commercial kitchens. With Haiou’s precision engineering, each machine ensures consistent texture, uniform thickness and effortless operation, allowing anyone to enjoy authentic noodle dishes without extensive experience or time-consuming preparation. Imagine preparing a variety of noodle types...

Key Drivers Impacting Executive Summary Reporter Gene Assay Market Size and Share CAGR Value: Global reporter gene assay market size was valued at USD 724.05 million in 2024 and is projected to reach USD 1480.20 million by 2032, with a CAGR of 9.35% during the forecast period of 2025 to 2032. Analysis and discussion of important industry trends, market size, market share...

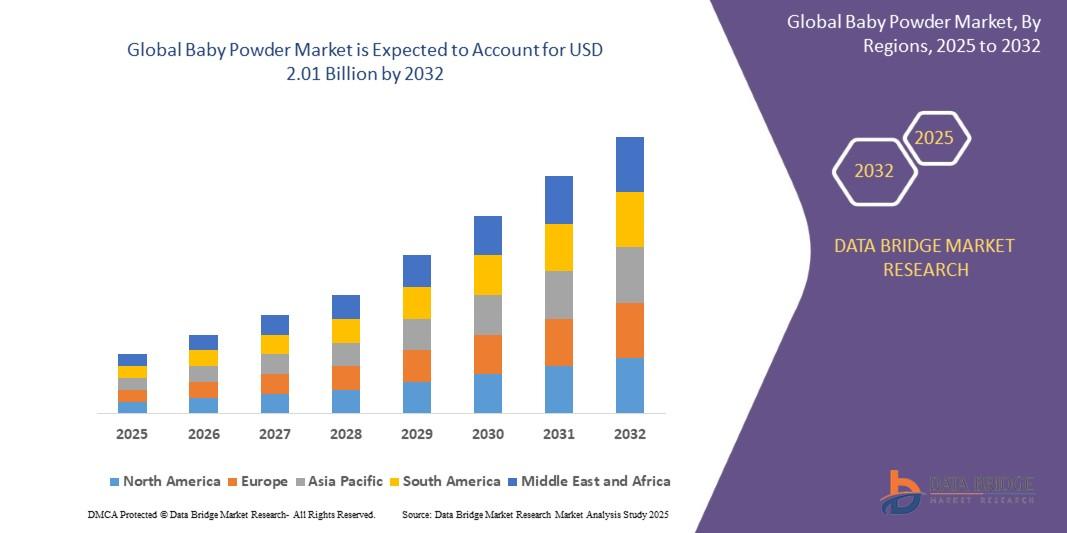

"In-Depth Study on Executive Summary Baby Powder Market Market Size and Share CAGR Value The global baby powder market was valued at USD 1.40 billion in 2024 and is expected to reach USD 2.01 billion by 2032 during the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 4.63%, primarily driven by easy availability of natural baby...