Commodity Price Volatility and Its Effect on Gold Mining Market

The global demand for gold continues to shift, influenced by emerging economies’ thirst for bullion, rising jewelry markets, and increased central‑bank acquisitions. Over the past few years, mining companies have experienced pressure to deliver more output while balancing environmental and social responsibilities. Under these evolving constraints, the Gold Mining Market is now more dynamic and unpredictable than before. A detailed Gold Mining growth drivers report reveals that key growth triggers include rising inflation, currency devaluation, increased investment demand from sovereign reserves, and growing consumer appetite for gold jewelry in developing economies. Together, these drivers paint a picture of growing demand, stressing the need for increased gold production globally.

Nevertheless, tapping this potential is far from straightforward. Many traditional gold‑producing regions are reaching deeper or lower‑grade ore zones, increasing extraction costs significantly. At the same time, regulatory compliance costs are rising, particularly in jurisdictions with strict environmental and labor laws. Additionally, companies need to invest in advanced mining technologies and tailings management — increasing upfront expenditure. For mines with no prior high‑grade reserves, the economic feasibility becomes marginal. These pressures make small and mid‑size mining firms especially vulnerable unless they adapt to new operational standards and secure long‑term financing.

This has led to a growing trend of consolidation and mergers within the sector, as larger mining houses absorb smaller firms to acquire reserves and optimize operations. By combining resources, expertise, and capital, such conglomerates improve their ability to navigate regulatory hurdles, invest in sustainable technologies, and deploy large‑scale extraction projects. Investors, too, are showing increased interest in well‑capitalized firms with diversified assets, strong compliance track records, and efficient production capabilities. The consolidation trend, if it continues, could reshape the global supply landscape, potentially leading to fewer but more powerful players.

Sponsored

Sponsored

Categories

- AI

- Design

- Fashion and Art

- Investment and Finance

- Top 10

- Christianity

- Climate and Enviroment

- Writing and Film

- Fitness

- Food

- Games

- Gardening

- Health

- Home and Interiors

- Marketing and Sales

- Music

- Making Money Online

- Others

- Books

- Religion

- Ecommerce

- Sports

- Cars

- Wellness

- Tech Gadgets

- Events

- Governments and Nations

- Science and Engineering

- Real Estate

- Travel, Tourism and Hospitality

- Education

- Startups

- Beauty and Cosmetics

- Agriculture

- Computer Operating Systems

- Crypto

- Politics and News

- Video Review

- Immigration

Read More

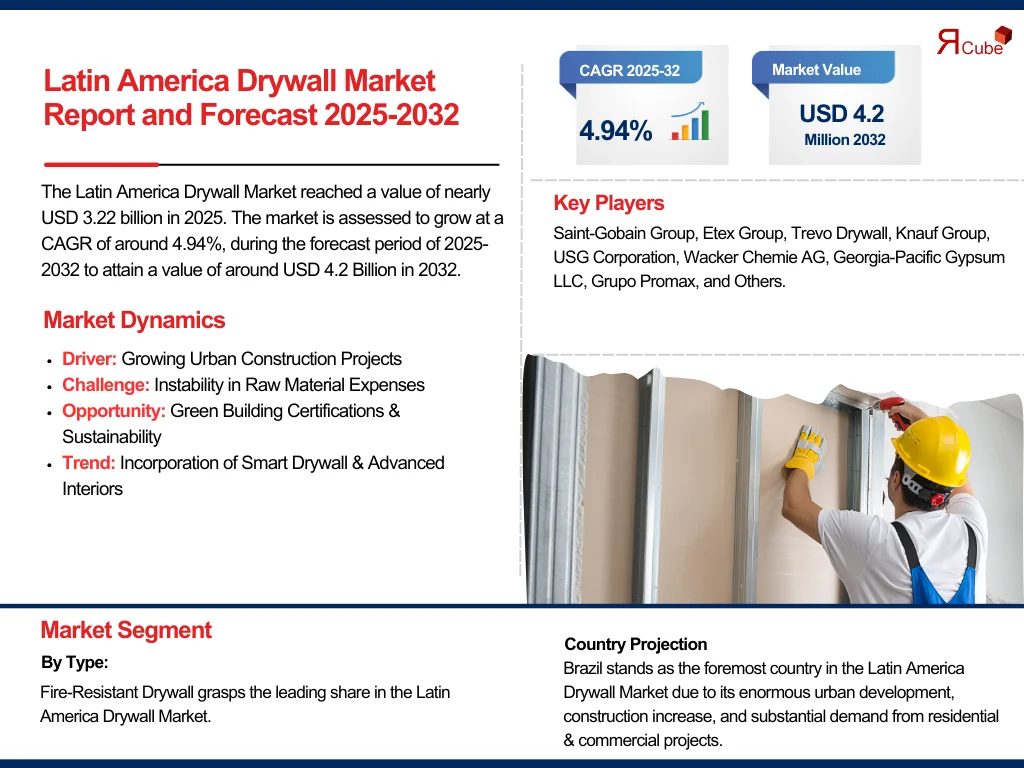

Executive Summary This report provides a comprehensive overview of the Latin America Drywall Market analyzing size, growth trends, key segments, and competitive dynamics. It highlights market drivers, challenges, and emerging opportunities while offering actionable insights for strategic decision-making. Historical data, current analysis, and future forecasts are included to help businesses...

According to For Insights Consultancy Automotive Sensors Market report 2034, discusses various factors driving or restraining the market, which will help the future market to grow with promising CAGR. The Automotive Sensors Market Research Reports offers an extensive collection of reports on different markets covering crucial details. The report studies the competitive environment of the...

Executive Summary Nasal Spray Vaccine Market Size, Share, and Competitive Landscape CAGR Value: Data Bridge Market Research analyses that the nasal spray vaccine market was valued at USD 122.287 million in 2021 and is expected to reach USD 250.91 million by 2029, registering a CAGR of 9.40% during the forecast period of 2022 to 2029. An exceptional Nasal Spray Vaccine...

Executive Summary Pass-By Noise Testing Market Opportunities by Size and Share The global pass-by noise testing market size was valued at USD 1.50 billion in 2024 and is expected to reach USD 2.80 billion by 2032, at a CAGR of 4.43% during the forecast period. An international Pass-By Noise Testing Market report lends a hand to identify how the market...

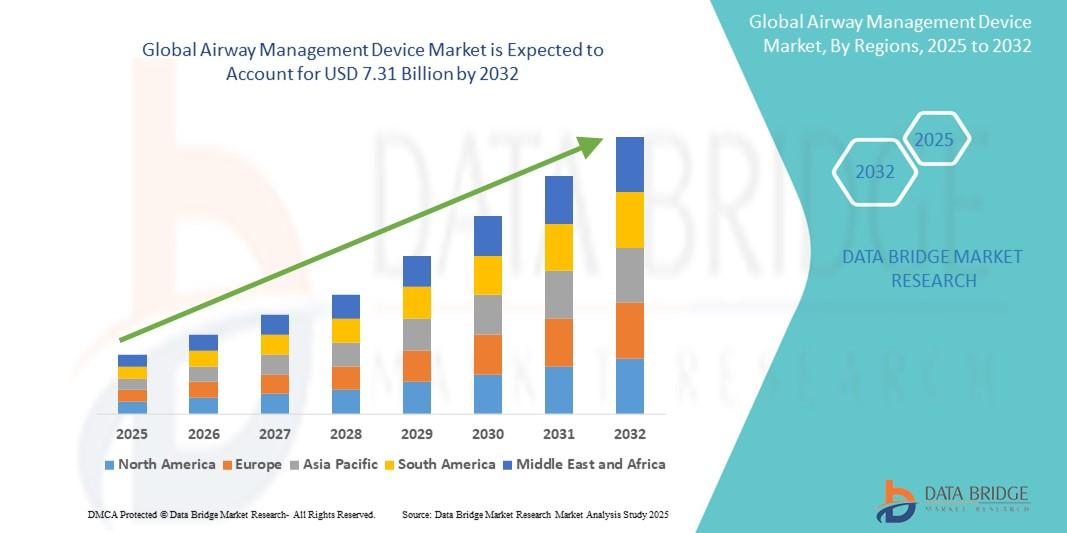

Future of Executive Summary Airway Management Device Market: Size and Share Dynamics CAGR Value The global airway management device market size was valued at USD 4.58 billion in 2024 and is expected to reach USD 7.31 billion by 2032, at a CAGR of 6.00% during the forecast period To thrive in this rapidly transforming marketplace, today’s businesses call for innovative and superlative...